Participant incentives are a common but often misunderstood cost in research administration. Confusion typically arises from the distinction between what is purchased and what is distributed. These steps have different implications, so many institutions separate them in financial workflows to ensure control and compliance.

Purchase: Creating Inventory

Often, participant incentives are not charged directly to a grant when purchased. Instead, they are acquired through an advance or holding account, typically a non-sponsored account such as a departmental or 2-ledger account. This account securely holds incentives until they are distributed.

For example, if 100 gift cards are purchased at $25 each, the $2,500 is charged to the holding account, not the sponsored project. At this point, no grant funds have been spent; the incentives are held as inventory.

Managing the Holding Account

To set up a holding account, an administrator requests approval from the finance department, specifying the purpose, funding source, and required amount. Once approved, all incentive purchases must be tracked as inventory using a log or spreadsheet that records each item’s serial number, value, and acquisition date.

As incentives are distributed, update the inventory log with the recipient, date, amount, and supporting documentation. Regularly reconcile inventory to recorded balances to ensure all items are accounted for. Address any discrepancies promptly in accordance with institutional procedures.

Why Incentives Aren’t Charged at Purchase

A common question is why participant incentives, especially gift cards, cannot be charged directly to a grant at the time of purchase. The answer comes down to both accounting principles and practical compliance.

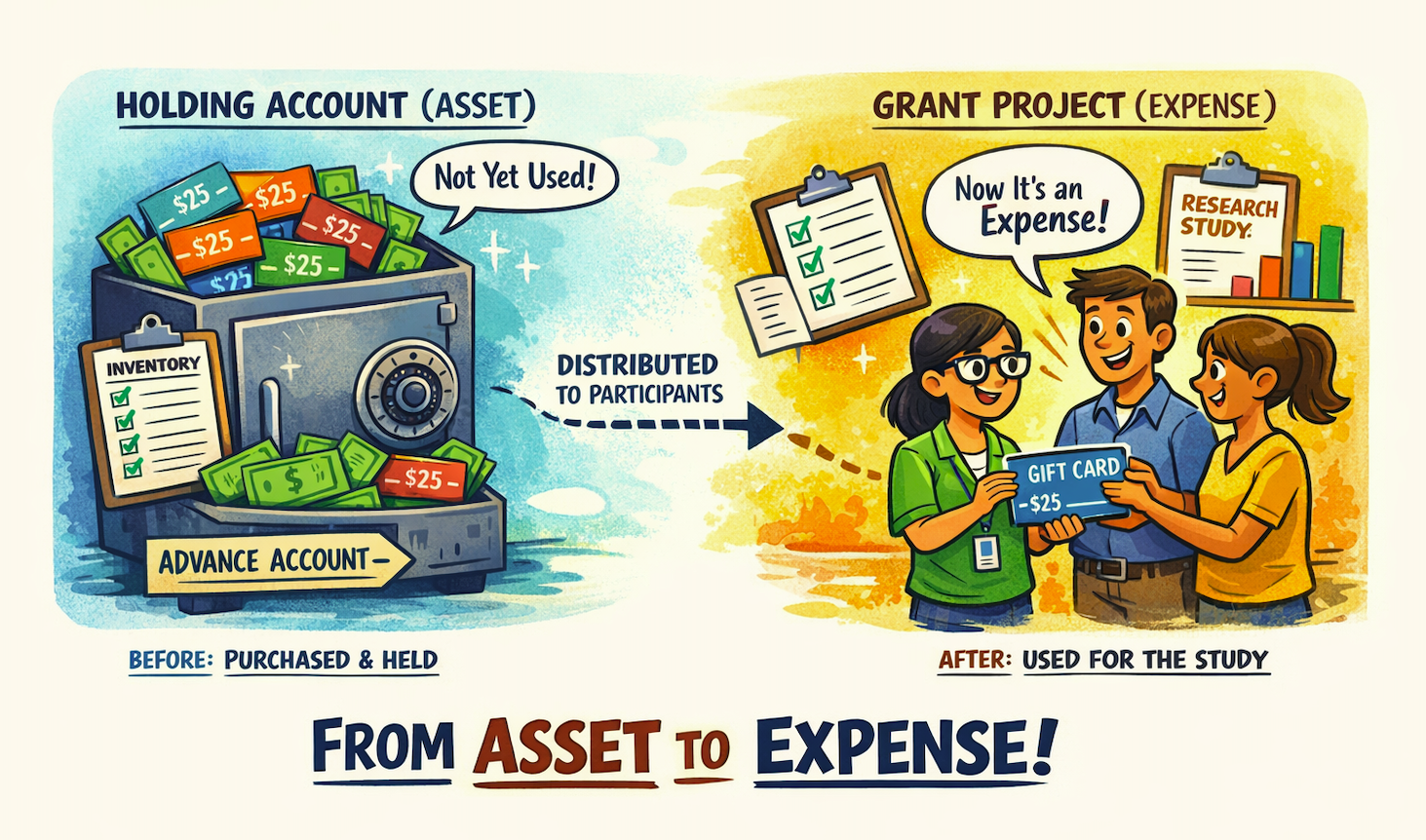

From an accounting standpoint, gift cards are considered an asset—not an expense. Under generally accepted accounting principles (GAAP), the purchase represents an asset that is still being held, not yet used. Because of this, the cost is recorded on an asset or holding account rather than expensed to a grant.

From an operational standpoint, no participant has received anything yet, and no research activity has taken place. This means the cost is not yet allocable to the project. It is a financial transaction, but not a programmatic expense.

Gift cards are also treated differently from typical purchases because they function as cash equivalents. Once purchased, they can be lost, stolen, or used without proper documentation if controls are not in place. Institutions, therefore, require a clear and defensible link between the expense and the participant activity it supports, and that link only exists once the incentive is distributed.

This creates a timing gap between when funds are spent and when they are truly earned by the project. Only when the incentives are distributed can the expense be recognized and charged to the grant.

A simple way to think about it is: until the incentive is used, it remains an asset; once it is distributed, it becomes an expense.

Required Documentation

Maintain documentation at each stage to support compliance and audit readiness.

The purchase and inventory stage should include purchase receipts, holding account approval, and an inventory log with serial numbers and values.

The distribution stage should include a log of recipients, dates, and amounts, along with signed acknowledgments or receipts when possible.

These records provide a clear audit trail linking purchases to research activity.

Example Tracker and How It Works

To make this process more practical, I’ve included an example tracker that reflects how participant incentives are managed across purchase, distribution, and expense.

The tracker separates inventory, distribution, and expense into distinct sections. Incentives are first recorded as inventory, then tracked as they are distributed, and finally tied to internal transfers once they are charged to the grant.

The goal is not just to track totals, but to reflect the full lifecycle of participant incentives—what has been purchased, what has been used, and what has been formally expensed.

Download Example TrackerDistribution: Creating Expense

The expense is valid and chargeable to the grant only when incentives are distributed to participants. At that time, only the distributed amount is transferred to the sponsored project, usually through an internal transfer such as a journal entry or interdepartmental transfer.

For example, if 100 cards are purchased for $2,500 and 60 are distributed, $1,500 is transferred to the grant, while the remaining $1,000 remains in the holding account as inventory.

Handling Remaining Incentives

Unused or expired incentives must be managed in accordance with institutional policy. Options include returning them to the department, reassigning them to another approved project, or disposing of expired items with proper documentation. Accurate records of remaining incentives are essential for reconciliation and project closeouts.

Purchasing creates inventory, and distribution creates expense.

The holding account stores inventory, and only distributed items are charged to the grant. This approach aligns financial reporting, operational tracking, and compliance.